Disclosure: Some of the links below are affiliate links, meaning, at no additional cost to you, I will earn a commission if you click through and make a purchase .

So, I’m debt free. What have we learned?

Here’s the deal. When it comes to obtaining credit and building debt, if you can think of it, I’ve done it… and that’s NOT a GOOD THING!

So, What can you learn from someone who has been in Neck Deep in Debt?

What NOT to do – that’s what!

Sign up for the 12 Step program here

Consolidation loans

The first time you’re granted a debt consolidation loan the skies open and the angels sing. There’s a huge weight lifted from you and all is right with the world.

Twelve months later – you didn’t change your habits or your lifestyle so now ALL THE CARDS are again maxed out PLUS you have the added burden of the loan payments.

You think that you won’t do that? Why? I did it – twice!

A debt consolidation loan is where a bank or finance company provides you with the money to pay off your outstanding debts and “consolidate” them (bring them all together) into one big loan. It sounds like the answer to your prayers!

There are advantages

- You only have one monthly payment to worry about;

- You often consolidate at a lower interest rate which saves you money;

- Your debt will be paid off in a set amount of time (typically 2 – 5 years);

- Any fees charged for this service are usually very low.

Banks and credit unions usually offer the best interest rates for debt consolidation loans. Many factors can help you get a better interest rate with a bank or credit union including your credit score, your net worth, whether or not you have a relationship with them and whether or not you can offer good security (collateral) for a loan. Good security for a debt consolidation loan will often be a newer model vehicle, boat, term deposit (non-RRSP) or another asset that can easily be sold or liquidated by the bank if you don’t pay make your loan payments.

For the past decade, banks have typically charged interest rates on debt consolidation loans of around 7% – 12%. Finance companies tend to charge anywhere from 14% for secured loans to over 30% for unsecured loans.

Disadvantages of a Debt Consolidation Loan

No security

Try getting any kind of loan when you’re mortgaged up to the hilt and own nothing that could be considered an asset.

Problems with Credit score

The more you borrow (and use) the worse the credit score. As with all lending, the provider of a consolidation loan needs to know you can be trusted. A poor credit score shows problems handling money and will negatively affect your ability to solve the problem. Start fixing your credit score with these simple to follow steps.

Income too low

If you made enough money you wouldn’t need to consolidate now would you?

That being said, banks aren’t morons. If you do have a decent income but have overburdened yourself then granting a consolidation loan means THEY get to collect all of the lovely interest that you’re currently paying to you vast Plethora of lenders and they can see that you are able to make those payments so, this could work. If it’s the opposite and you simply do not make enough to survive, which is usually why you’ve turned to credit, then this is where the vicious circle starts.

Too much debt

Once you’re too far in then even a consolidation won’t save you. That’s when you throw up the white flag and make the calls. My advice (for Canadians) is to start with your local office of 4 Pillars.

Maybe head over to Life after Debt to understand more about WHY I recommend 4Pillars.

Balance transfers

So, there’s a shiny new card offering 0% on balance transfers which means you could make your payments for the next year and actually attack that principal amount outstanding. Sounds great.

Did you close the account that’s now at nil (after you transferred the balance)? No?

So – you’re keeping this nice, empty card for what…an emergency? Addicted to credit much?

The terrifying side to balance transfers is that you are left with a completely clear, still open for use, credit card. If you haven’t addressed your relationship with money and curbed you’re need to purchase All The Things then, (and I don’t need a crystal ball for this next part), the first commercial for a “Sunny Destination” that you see will have you convincing yourself that it’s a great idea to take a break and relax before you get back to the daily slog of life and the promise to clear off that new consolidation loan. You may even build a budget that shows how responsible you’re going to be when you get back from vacation. Plotting the payments to the (previously) empty card and forgoing the latte’s to make everything balance.

Please Don’t. Please don’t. Please don’t.

HELLO: My name is Anna and I’m addicted to credit.

I’m not going to go into how many times I did this with my credit cards. Getting everything cleared and amalgamated into one (long term) loan and then racking up my cards all over again. It doesn’t take long, believe me and you’re right back where you started.

I never, ever closed a single account after I’ve cleared it…just in case. This is the single biggest mistake anyone can ever make but, when you’re addicted to credit you justify it to yourself.

In some instances, rolling over your debts can come back to bite you. Aside from hidden fees and unpredictable interest rates, balance transfers can even harm your credit score and increase the cost of future borrowing.

Over compensating: Presents instead of Presence.

Anyone else go on guilt trips? In the past I tried to keep my kids entertained in the car and in hotel rooms with Junk food (their favorite – Go Figure!) and with toys then games (of the PS / Nintendo kind- so, not cheap). This usually happened because I worked 24 / 7 and needed to get them from school to “somewhere safe” until I finished The__________(insert never ending work crap here).

When I did take down time I usually liked to treat them to a movie or a trip to the mall. I say that was for them but really – you have one day off, do you want to stay at home and look at the state of your house – which you are also neglecting? Who doesn’t love dinner and a movie?

By the time you get to a Day Off you feel like you deserve a treat too so, what’s wrong with a quick (45 minutes and over $300 later) stop at Sephora while you’re there?

Redressing the balance and rebuilding the relationships.

In the past three years I’ve worked at rebuilding a relationship with my kids, paying attention to them and listening when they speak instead of checking emails and taking calls. It’s not perfect but it is better than it was.

My little guy (he’s 6 foot tall now) still tries to wheedle cash or computer games out of us but, now that we set goals for rewards, there’s a sense of achievement and camaraderie in what we do. The current project is weight loss and my son is money motivated!

I used to justify my decisions (to work late or on the weekends) based upon my own childhood. Adults never paid us kids any attention. We were left to come up with our own entertainment. There was one Cartoon on per day so TV was never interesting (1970’s England). My siblings and I just did our thing. No need for adult attention or things to keep us occupied. No wonder people say life was simpler then. There wasn’t eleventy billion parenting guru’s all out there telling you how wrong you were getting everything and messing up your kids lives!

Live an Instagram lie, sorry, Life

Try as I might I just can’t get behind Instagram and the LIES it tells. I’m sure there’s the odd one or two out there that really do live #soblessed lives but really? Give me a break.

I refuse to look at all of these perfect pictures of perfect lives and buy into the fact that #everythingISperfect and #havingthetimeofmylife. So much bullshit here and the falseness behind each fake pout makes my blood boil. OK – I’m not very photogenic either so it may be a little bit of jealousy too but, do these so called influencers consider for one second what they may be doing to people who #wannabejustlikeyou?

I see girls spending thousands on the latest purse by “——-designer—-” because it was featured on their favorite influencers site with no regard to the future repercussions of what debt they’re building for themselves now. These impressionable minds (I don’t care if you are 23, I’m way older!) feel important and “worthy” when they can imitate a top influencers style, living vicariously through Instagram endorphins; posting pictures where they look good, in swanky surroundings, laughing joyously. How many attempts did it take to get that picture just right?

Meanwhile, back in their dingy London flat, it’s Ramen for dinner…again.

Think you can fix this…alone

Good luck buddy. This is bigger than just you.

Once you have tried one consolidation loan and now you’re back where you started that is the time to take a long hard look at your life and try to figure out why you keep doing this. What are you compensating for?

Time to invest in some help, before it’s too late.

Start with my free 12 step program to recovery. It’s designed to take you through the stages of gaining control over your spending and assessing the mindsets behind why you’re doing what you’re doing.

If you’re too far gone for even this (as we were) then call in the professionals. (4 Pillars.ca)

Believe this is only happening to you

Bless. Really? Try this on for size:

“…about 8 per cent of indebted households owe 350 per cent or more of their gross income …” Bank of Canada.ca

It is easy, given the total secrecy that we envelope our debt problems in, that you may believe this is only a problem for you. If that were actually the case then there would be no need for collection agents and debt relief programs and the Bank of Canada wouldn’t have been keeping a watchful eye on what’s going on for the past several years. They’re scared… so we should be too.

Look at what just happened in the US. The longest Presidential shut down in history. The TV screens were filled with people sobbing hysterically that they couldn’t pay the rent or buy food, never mind pay their bills! This was a very real situation happening to real people across the country and these people are just like you and me.

You are not alone and there are people out there just like me who want to help.

Ignore lenders

This is a BIG mistake. Big! Huge!

Without communication things escalate pretty fast. That doesn’t mean that, just because you do communicate, things won’t escalate but at least you will know that you tried.

In the early days we spoke with all of our lenders and explained our situation (job losses) and were shell shocked by the callous, often rude way we were spoken to. Of course, we now know this was just some telephone gnome paid pennies on the dollar to take the first call and play hard ball. Straight away – ask to speak to a supervisor. The initial contact person has zero authority to help you in any way. Once you reach a supervisor, request their manager. Put all of this in writing too and dictate your terms of communication. If you’re happy for Visa to call you put pressure on you for missed payments then OK. If you would rather have an email then say so! Forbid the telephone calls but do so in writing.

Let all of your lenders know what you can and can’t do (make a proposal). Ask for assistance but be specific. Do you want a payment holiday? A freeze on Interest? Something else?

The lender won’t make the first move towards a solution so do your homework.

Keep digging – reward your irresponsible behaviors.

So, things aren’t quite so bad for you yet but you can see the day when the cards are maxed out and you won’t be able to get them paid back and it’s not so far away? When you focus on this dark future it makes you sad, anxious, depressed and so, to cheer yourself up you go online (or head to the shops) and get that “..whatever..” you’ve had your eye on?

Retail therapy is not a solution to anxiety or depression. Give your head a shake. You are just setting yourself up for a massive failure. Do you hate yourself so much that you would deliberately sabotage your future?

This isn’t easy for me to write because this is what I did. New clothes to look the part I was trying to play, to compensate for my (perceived) inadequacies of a female auditor in a male dominated world of finance. Flashy car to give the appearance to my old friends (back in the poor part of town) that I was successful. My great job was worth the extra years of school (something I was once ridiculed for by an uneducated friend with three children by the time she was 20).

Dinner out (because I can’t actually cook and admitting to this I would also have to confess that I can’t cook because I was never taught, as my Mom was never taught). This would open up a can of worms behind my background and uber poor upbringing on the council estates (substitute trailer park made with bricks and mortar instead of trailers) of England. This did not fit with the persona I was portraying. No!

How about booking three vacations a year with my (then) boyfriend (who came from money) and never admitting that I couldn’t afford the same lifestyle that he could.

I only learned my lesson in 2016 (and I started on my road to ruin in 1987). Now, I know why I did the things I did and I am no longer trying to be something I’m not. To be honest it was exhausting.

Procrastinate

You think that if you can just make it to Friday, Payday, the end of the month, then you can figure out a solution. After all, you’re not broke. You have a paycheque coming. It’s all a matter of timing.

Sorry. I’m actually laughing here because I re-read this and it came out in my actual voice. This was my misconception. I have time to sort this out so put it off until….

Not so my friend. The day will dawn when the time is up. By then it will be too late for options.

Lifestyle ooze – make more, spend more

Ooh! My favorite waste of time and money.

Get a pay raise. Change the car.

Receive a tax refund. Book a vacation.

Extending your lifestyle to take up the slack that the extra money can afford you instead of getting out of debt or investing for your future. Great while it lasts but..it doesn’t last!

The Good stuff

So – I’ve been there; Done that; Bought the T-shirt.

What can I offer you from this vast experience?

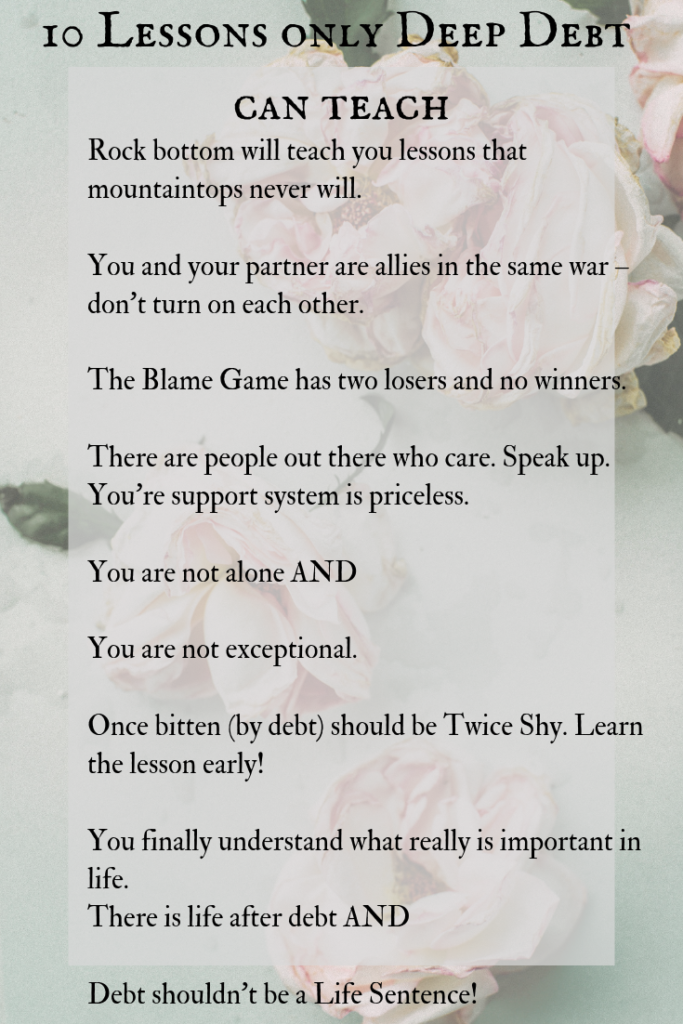

My 10 Life Lessons:

There is a solution to this available now. It wasn’t around when I needed it. Go take a look at MASTER YOUR MONEY, Download the free Ebook (limited time only!!). Once you’re ready to finally get serious then please, go sign up for my 12 Step email program to being Debt Free.

Hi Anna,

All great advice! Debt has taught me some hard lesson and now I choose life! I’m 3 months away to being 100% debt free and boy does it feel GOOD!

Also, I’m right there with you on the whole social media “my life is perfect” lie! I was so over that years ago!